Government debt levels have reached an all time high with US government debt at $37 trillion in debt and the UK is £3.1 trillion ($4.2 trillion) in debt.

You live somewhere else? Your government is probably in record levels of debt as well!

But what does that actually mean for you?

To answer this question, we need to know three things:

- What is government debt?

- Why it is needed?

- How it is borrowed?

- Where does the money end up?

Without government debt, schools would have no teachers, pensioners would be homeless and we’d probably be living in the Third Reich (or lost World War 2). Yes, governments around the world borrowed heavily to finance the war efforts).

Government debt is taken out when governments spend more money than they make. While governments do make billions in taxes, they don’t quite make enough to cover all their spending on expenses such as healthcare, defence, education and social security (state pensions).

Governments make up the shortfall by borrowing from entities such as corporations, investment/pension funds, insurance companies, foreign governments, commercial banks and most crucially, central banks such as the Federal Reserve or the Bank of England.

Much of the money borrowed by the government goes to its own people. For example, if your government decides to reduce your taxes (like the UK did with National Insurance Tax in 2024), it’ll leave more money for you to spend. In turn, the government would lose out on that tax revenue and borrow the difference. This applies across all sorts of government activities such as lowered trade tariffs, increased pensions and corporate tax cuts (as these encourage companies to invest more in the country, creating new tax revenues and thousands of jobs for its people). At the end of the day, our governments borrow money and put it in our pockets.

More government debt = more money for its people = increased household wealth

Although chances are, you probably don’t see much of that increase in household wealth.

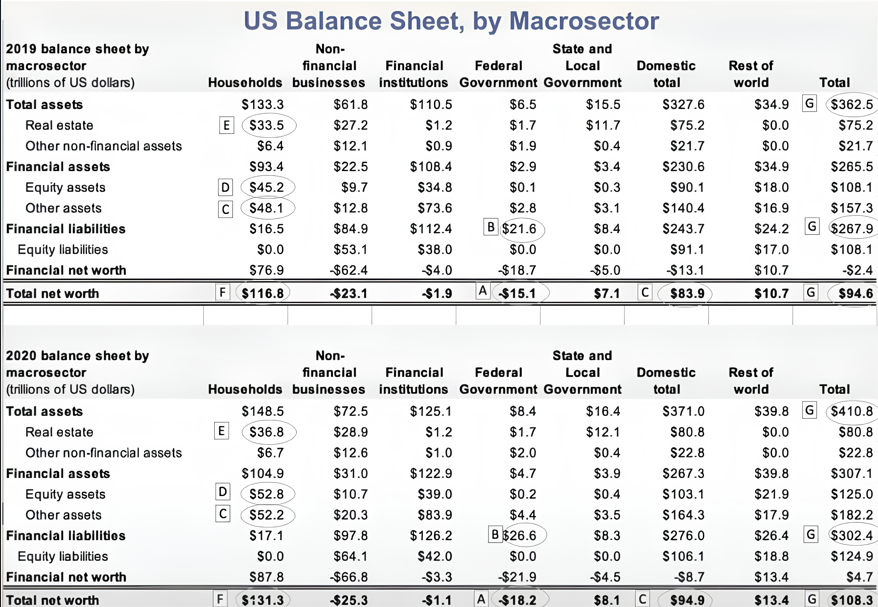

To help explain why, lets take a look at what happened when the US government borrowed at record levels between 2019 and 2020 during the COVID-19 pandemic.

By looking at the things that make up the net worth of the US government, we can see that the US government was worth $3 trillion less in 2020 than it was in 2019 . So the US government borrowed a record $3 trillion in 2020. In the meantime, US household wealth increased by almost 5 times that amount ($14.5 trillion).

Most of that increase came from stocks and real estate (property), which contributed a $10 trillion increase in household wealth.

To find out why why stocks and real estate soared in value during this point in time, we need to take a quick dive into where money flows and how it changes during high levels of government borrowing.

Remember that $3 trillion that the US government borrowed? The government borrowed that from the central bank (the Federal Reserve) which got its money by ‘printing’ it because it is allowed to do so. (By the way, when I say printing, the central bank adds money to its account electronically.)

$2.2 trillion of that borrowed money went towards stimulus payments which protected people’s incomes while businesses shut down during the COVID pandemic. Otherwise, they’d have been left without food or shelter. So as expected, people used most of that money to pay to continue paying for their essentials such as food, rent, utility bills, and maybe a few non-essentials. The key difference here is that the all of the money that people spent was borrowed out of thin air, this put more money into the economy.

So there’s more money in the economy, yet the average person has spent most of it, so where did the money end up? That’s right, it ended up in the hands of the very people that own the houses, commercial properties, oil, gas and utility companies, supermarkets and more. In other words, the extra money went to the people that owned assets. Now these people tend to be quite wealthy, so they have nothing better to do with that money (especially during covid) than to buy even more assets; this increased demand which skyrocketed property and stock prices.

Here’s why didn’t see an increase in your wealth during that time – the bottom 60% of us only own 10% of real estate and stocks. Most of us don’t benefit from increases in property and stock prices. The top 10% who own 93% of all stocks however, saw their wealths skyrocket, with the world creating a record-breaking 500 billionaires in 2021.

Increased government debt drives wealth inequality.

So while government debt does increase household wealth in all economies, the average person that owns little to no assets (probably you) will never their wealth increase.

However you will bear the cost of government borrowing. As governments borrow more, asset price inflation will mean that the house you’ve always wanted will be become ever more unaffordable. To make matters worse, the government needs to pay back the interest on the money borrowed, which falls on the shoulders on all taxpayers through increased taxation in the future. The UK is already seeing this play out, with debt interest costs at record levels and tax rises being hinted at for this autumn.

So now we know how government borrowing makes the average person poorer, what can you do to escape?

The governments aren’t going to stop borrowing any time soon, so there is only one answer – join the rich and invest in assets such as stocks and real estate .

However for most people, it is easier said than done (everyone would be doing it otherwise). There are a lot of obstacles for most people to even get started.

That is why I’ve set out to educate people on how they can set themselves up for a successful future in an increasingly expensive world.

Life is not easy, but it certainly will be.

Leave a Reply